Australia

Australia China

China India

India Indonesia

Indonesia Japan

Japan Malaysia

Malaysia Philippines

Philippines Singapore

Singapore South Korea

South Korea Taiwan

Taiwan Thailand

Thailand Vietnam

Vietnam

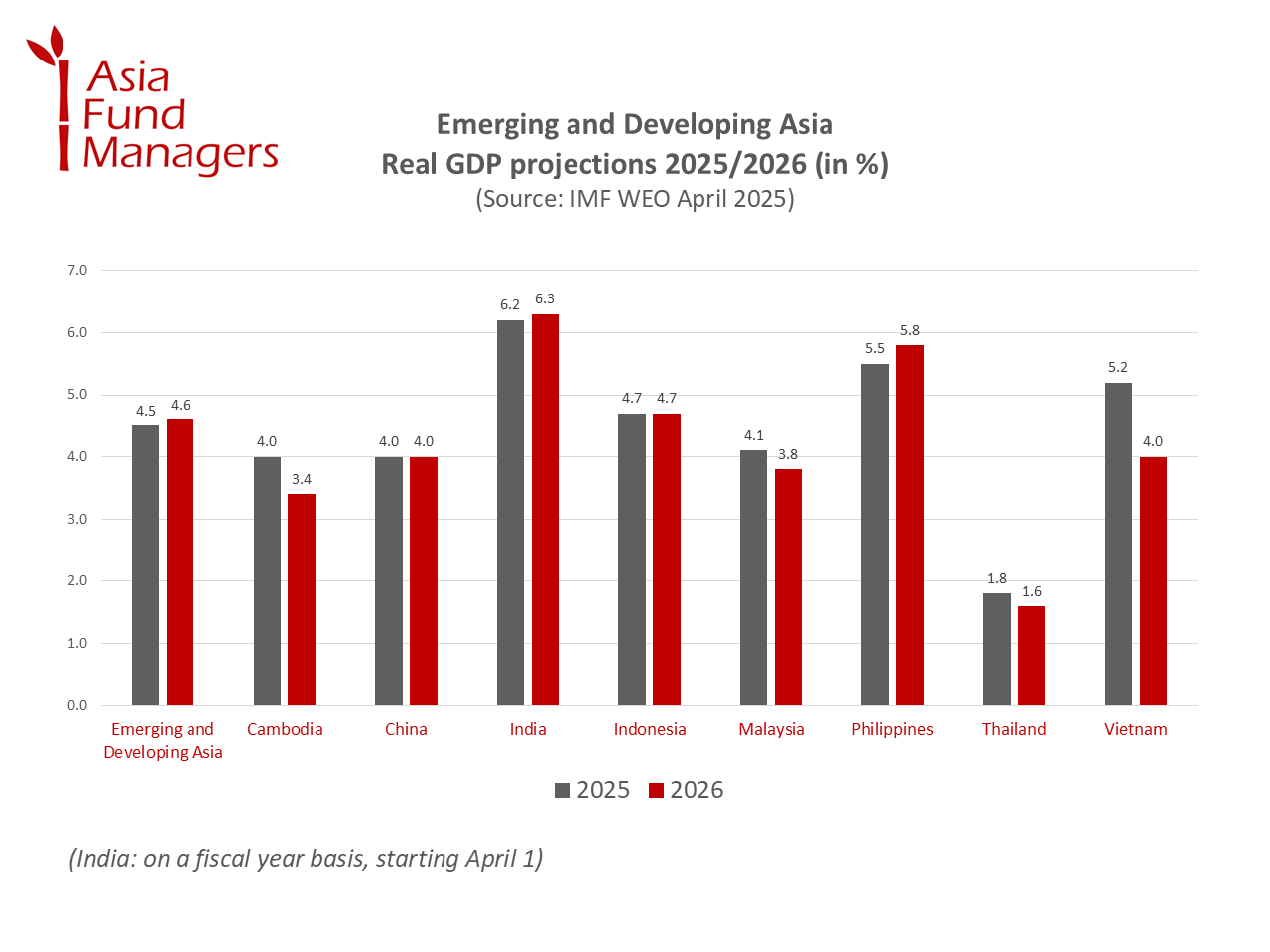

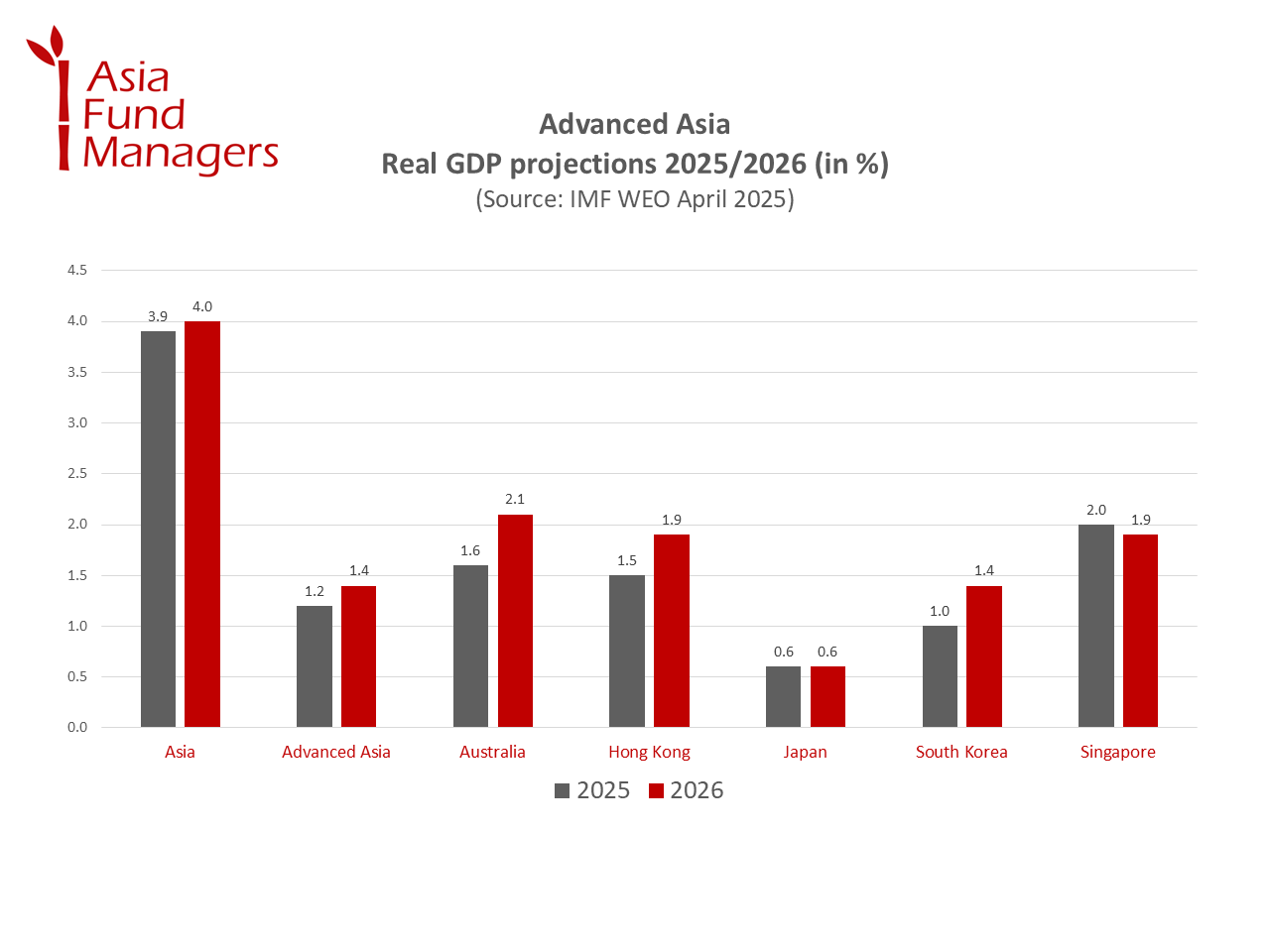

The International Monetary Fund’s latest Regional Economic Outlook for Asia and the Pacific, released in April 2025, paints a mixed but cautious picture for the region. After a strong rebound in 2023 and relatively resilient growth through 2024, Asia’s economy is now facing a pronounced slowdown. According to the IMF, regional growth is projected to decline from 4.6% in 2024 to 3.9% in 2025, reflecting mounting global and domestic challenges. Compared to the World Economic Outlook (WEO) of October 2024, it is a downward revision of 0.5 percentage points and the IMF’s sharpest since the pandemic.

Slowing momentum amid rising global uncertainty

The IMF’s downward revision of Asia’s near-term outlook is closely tied to a deteriorating global environment. “Lower external demand, a soft tech cycle, and subdued private consumption in several countries will weigh on activity,” said the IMF.

In particular, the recent trade policy shocks are weighing on the Asia’s economy outlook as the region has high exposure to global supply chains.

The trade tensions are particularly concerning for export-oriented economies such as China, South Korea, Taiwan, and ASEAN nations, where manufacturing and electronics exports heavily depend on stable trade flows. The softening in the global tech cycle has further dampened prospects for the region’s high-performing tech sectors, with semiconductor-heavy economies already seeing a contraction in export volumes, according to the IMF.

“Asia’s export-led growth model delivered unprecedented prosperity. But the world has changed. Trade is more uncertain, government budgets more constrained, and domestic demand more important than ever,” wrote Krishna Srinivasan, the IMF’s Director of the Asia and Pacific Department, in a blog article.

Asia economy outlook: inflation in check, but growth risks remain

While inflation has largely normalized—falling within central bank targets in most countries—private consumption remains subdued across much of the region. The IMF notes that consumer confidence has not fully recovered, especially in economies where households are still dealing with the aftereffects of the COVID-19 pandemic and elevated debt levels.

China’s economy, which has been a cornerstone of Asia’s growth story, continues to face headwinds. While growth remains stable, structural challenges—such as the ongoing property sector correction and weak household consumption—are weighing on domestic demand. The IMF projects China’s growth to slow from 5% in 2024 to 4% in 2025 and 2026, contributing significantly to Asia’s overall deceleration. This is a downward revision from the last WEO from 0.5 and 0.1 percentage points, respectively.

Also, India’s growth outlook was revised downward by 0.3 and 0.2 percentage points, respectively. The IMF now expected the South Asian economy to grow 6.2% in 2025 and 6.3% in 2026, down from 6.5% in 2024.* This revision is smaller than that of other countries, as India is less exposed to trade shock.

Growth in the ASEAN sees a steep downgrade of 0.6 percentage points to 4.1% in 2025. The IMF cites external shocks and domestic demand weakness in some economies like Cambodia and Vietnam. as reasons.

Amongst the advanced Asian economies, South Korea and Hong Kong saw the steepest downgrade of 1.2 and 1.5 percentage points, respectively. South Korea is expected to grow 1.0% in 2025 due to heightened global trade tensions and domestic policy uncertainty. For Hong Kong, the IMF sees a 1.5% growth.

“Risks tilted to the downside”

Overall, the Asia economy outlook for 2025 has become more clouded, with trade tensions, slowing external demand, and weak domestic consumption taking a toll on growth prospects.

“Risks are tilted to the downside in the face of the region’s greater vulnerability to the uncertain trade environment and weaker-than-expected global demand as well as asset price volatility increasing the potential for disrupting capital flows and investment,” said Srinivasan.

“Embracing smart policy choices will help Asia write the next chapter of its growth story—not just as the world’s factory, but as a dynamic, resilient, and integrated economic power,” he concluded.

*by fiscal year, starting April 1.